Wealthstead pulls every account you have into one private desktop app. It shows the asset mix you actually hold, turns the mix you want into exact Add / Reduce moves at each broker, and stress-tests the retirement that follows — with three independent projection models that show their work. No brokerage logins. Nothing uploaded. A calculator for your own plan — illustrative, never advice.

If you manage your own portfolio, you've probably hit all three walls.

Six accounts, two brokers, one hand-built spreadsheet. Every statement means re-typing, re-linking, re-checking a formula you wrote years ago. You maintain the tool instead of the plan.

Your portfolio tracker says you're 4% overweight equities. Fine — which fund, in which account, by how many dollars? It goes quiet exactly where the work begins.

A planner hands you "94% success" and won't say which assumptions drive it, or how a different reading of history would score the same plan. One confident number, zero visible knobs.

Wealthstead replaces all three with one loop — five plain questions, answered on your own machine, from your own numbers.

The same loop an advisor runs — see it, shape it, act on it, fill it with the right funds, project it — except you keep the judgment, the data, and the fee.

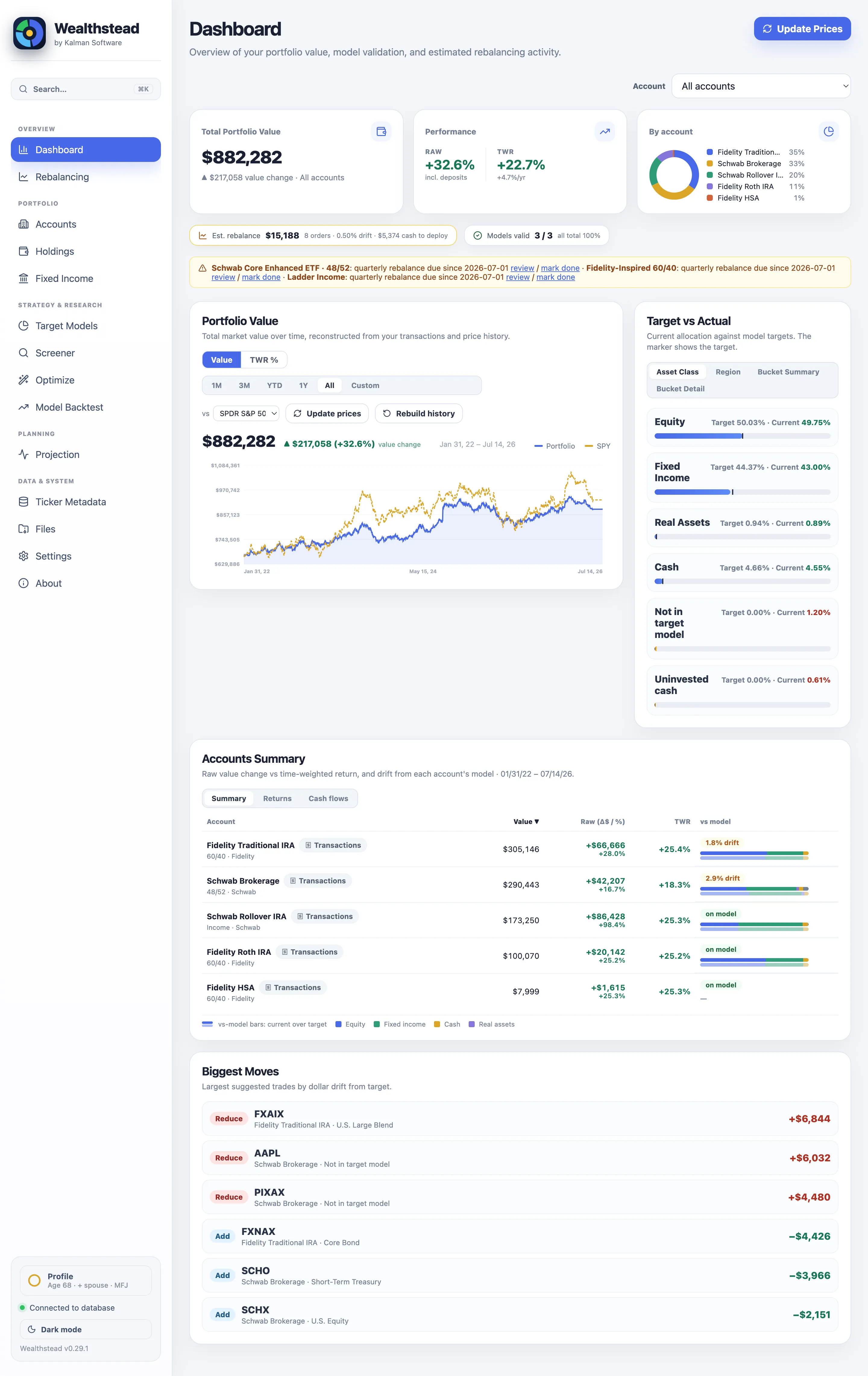

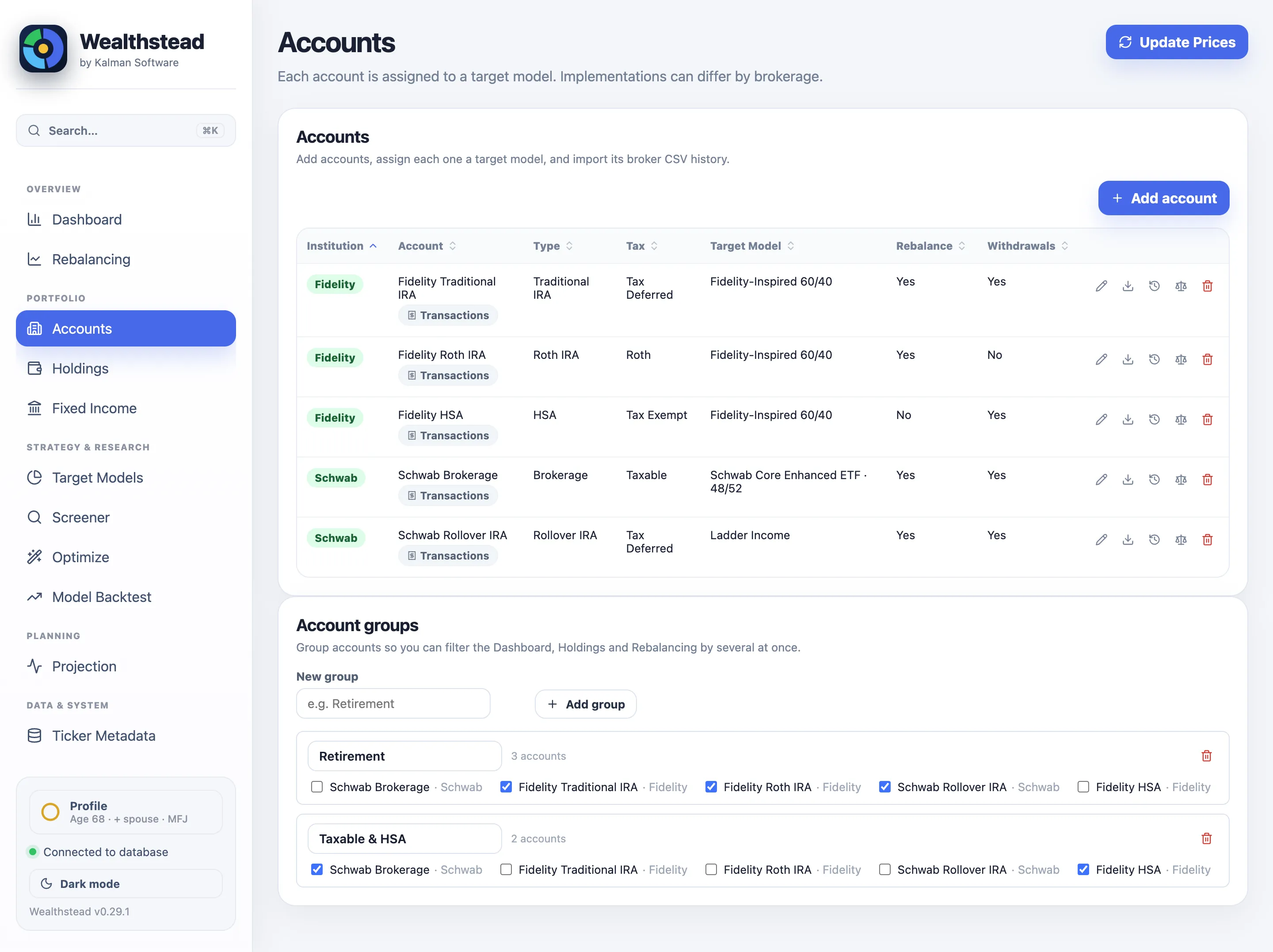

Bring in every account you have — workplace plans, IRAs, the TSP, the taxable brokerage — and get one honest picture. Two ways in, and both stay entirely on your machine: type in your monthly statement, or import the CSV your broker already exports.

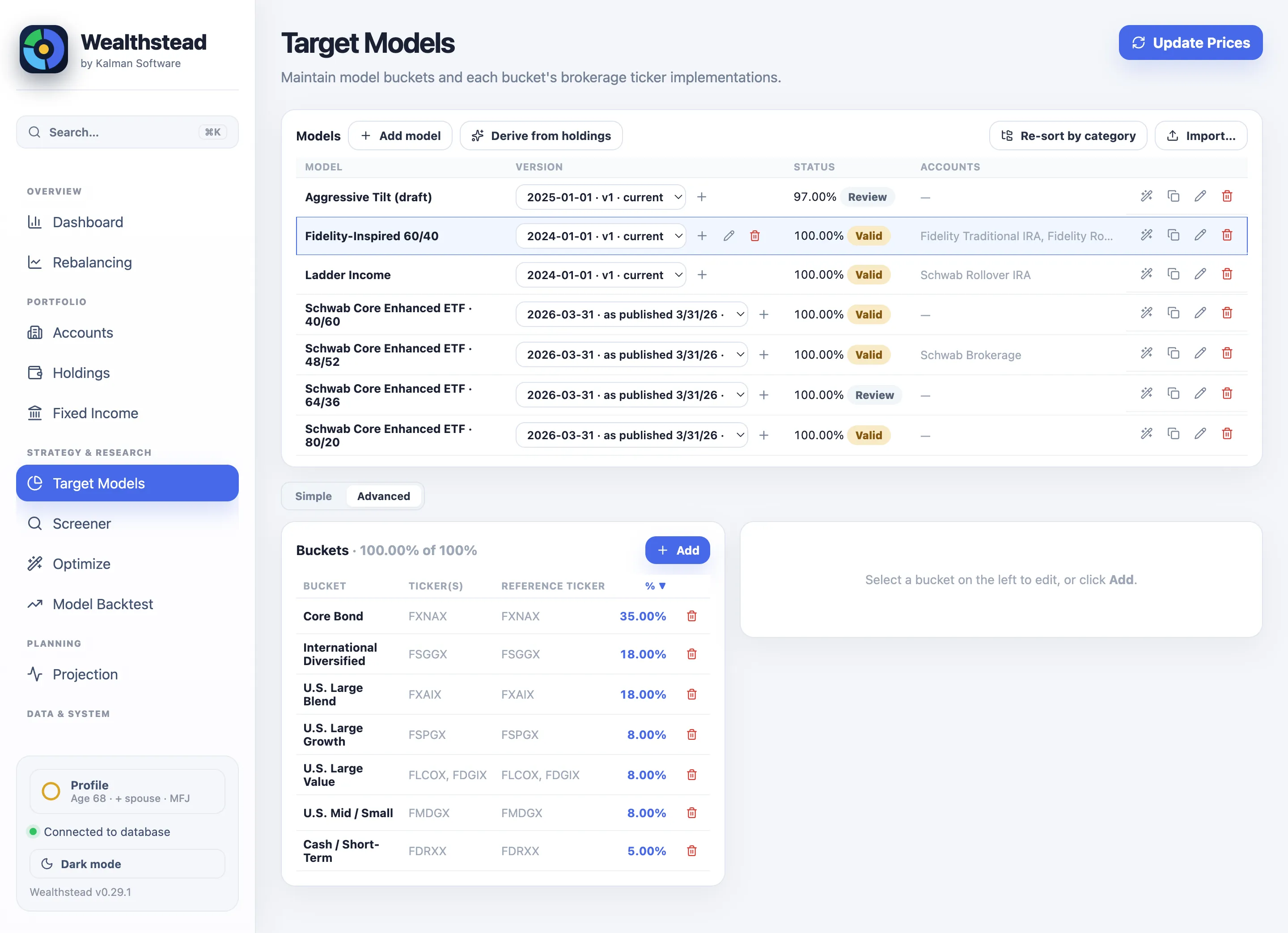

The moment your holdings are in, Wealthstead classifies them into asset-class buckets and shows the allocation you actually hold — across everything, not per account. For most people it's the first honest look in years: the legacy stock, the overlapping funds, the 70/30 you thought was 60/40. Then you design the mix you want.

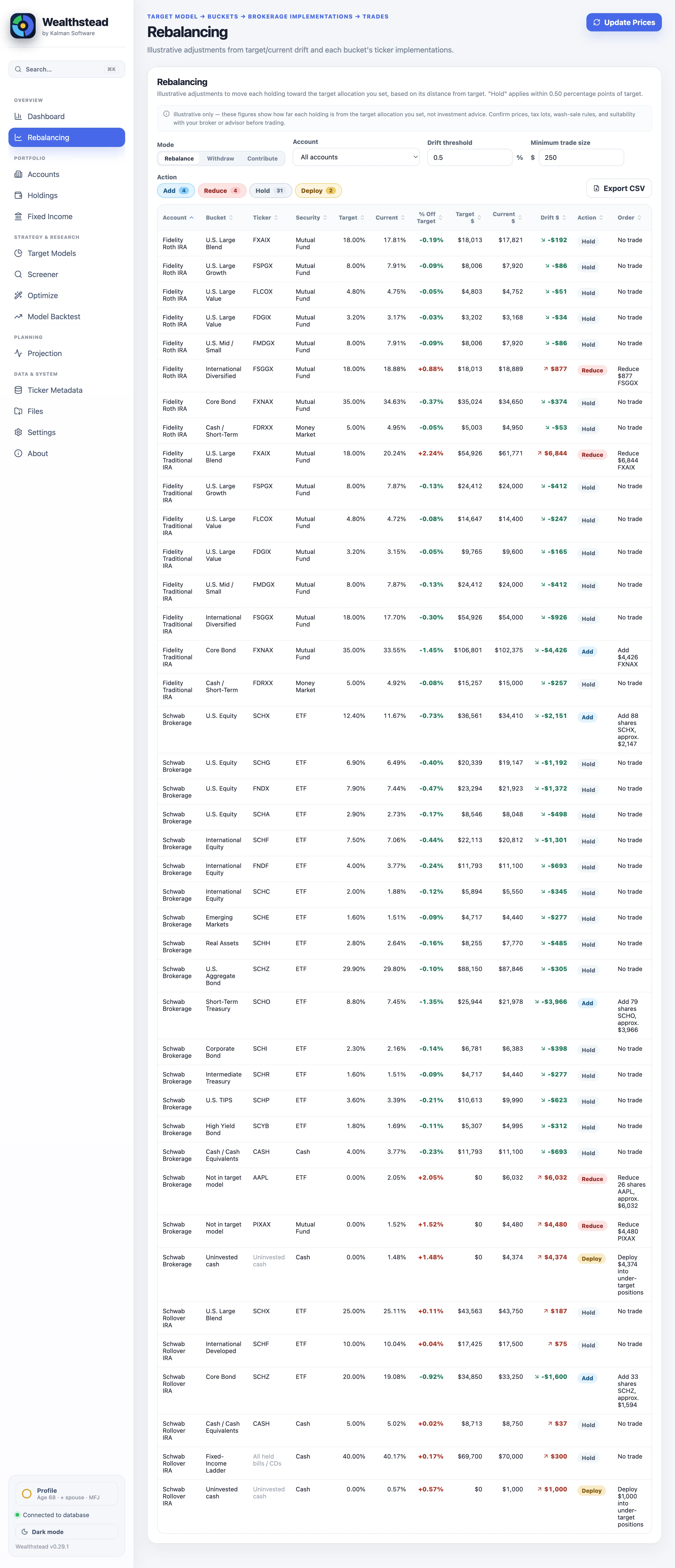

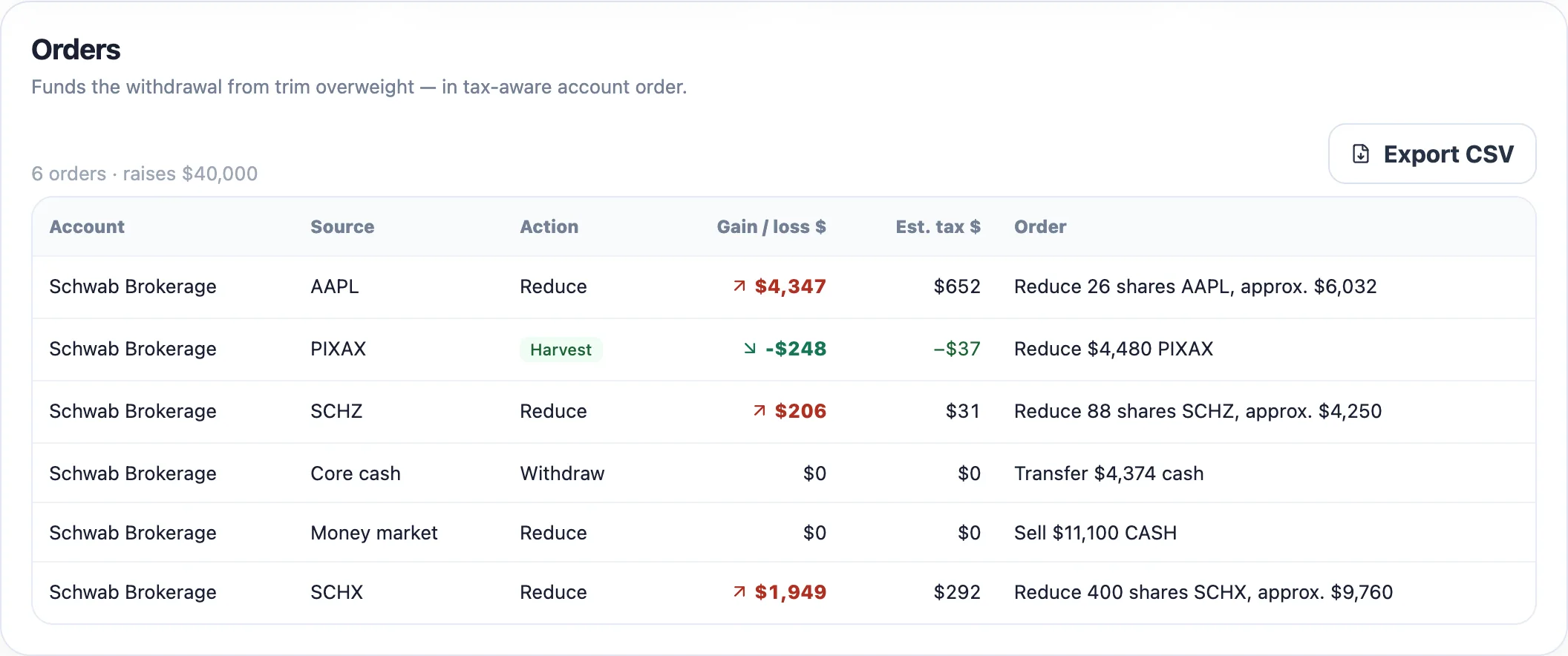

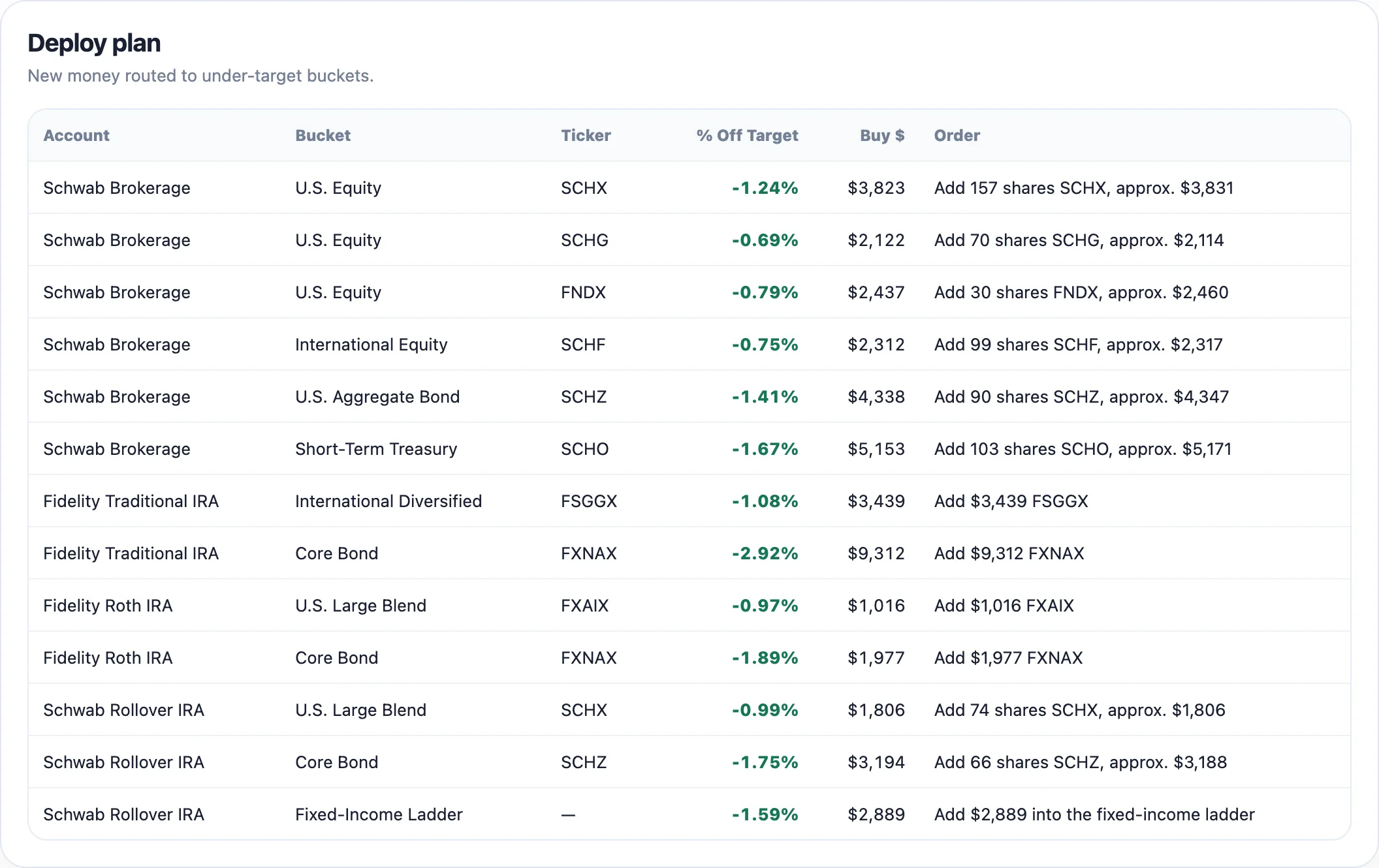

This is where trackers stop and Wealthstead starts. Drift becomes a clear list — Add this, Reduce that, to the dollar, per account — funds in dollars, ETFs in whole shares, and anything inside your drift band stays a Hold, so noise never becomes churn. Point the same engine at new cash or a withdrawal and it writes that plan too.

Every account, bucket and ticker classified Add / Reduce / Hold — brokerage-aware, off-model holdings queued to exit.

Raise cash tax-aware: lot-level gain/loss, estimated tax, and Harvest badges where a loss can be booked.

Enter new cash and get an add-only deploy plan that closes your largest gaps first.

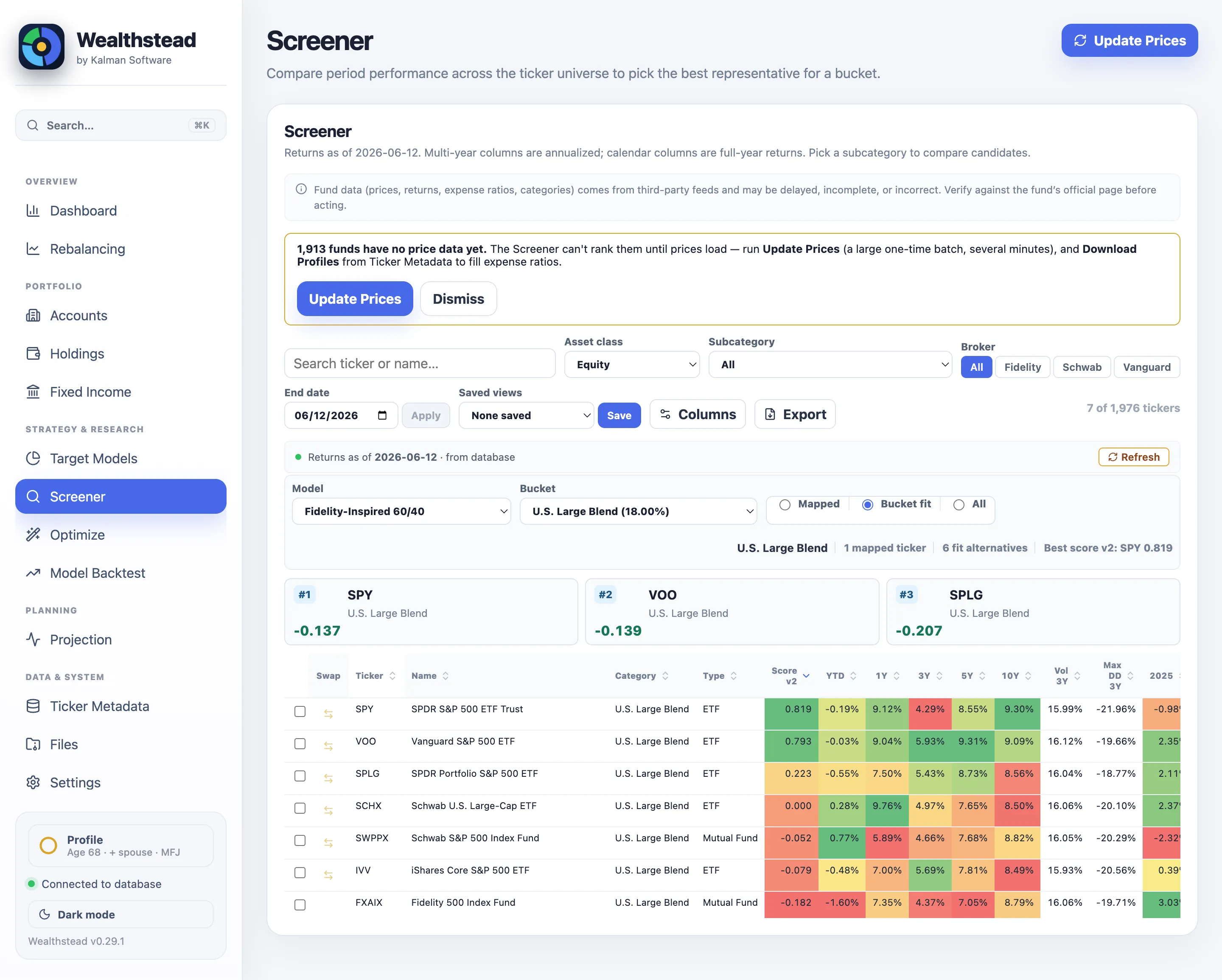

Keep the workflow you already trust: run Fidelity's or Schwab's fund screener, pick your categories, check ETFs and no-transaction-fee funds — because paying a fee every rebalance is how good plans die. Then bring the candidates into Wealthstead and let the evidence sort them.

Trailing & calendar-year returns plus risk, green to red, ranked by a tunable, Sharpe-like Score.

Narrow to one sleeve — "U.S. Large Blend" — and see SPY / VOO / SPLG / SCHX scored and graded Exact / Close / Broad.

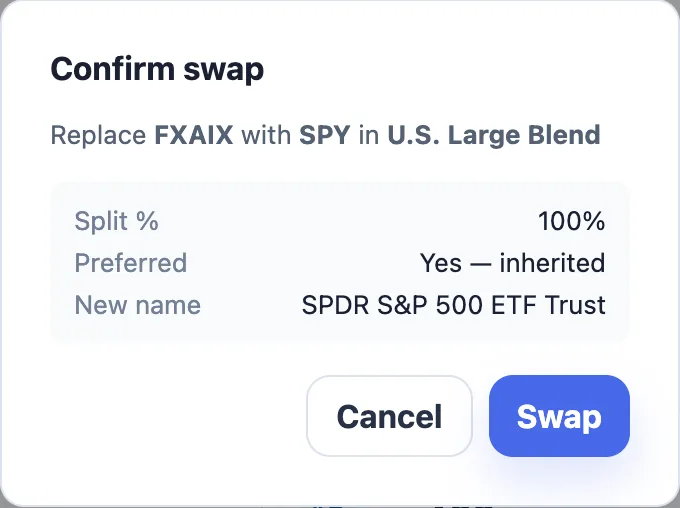

Confirm the swap and the model updates in place — screening and editing are one motion.

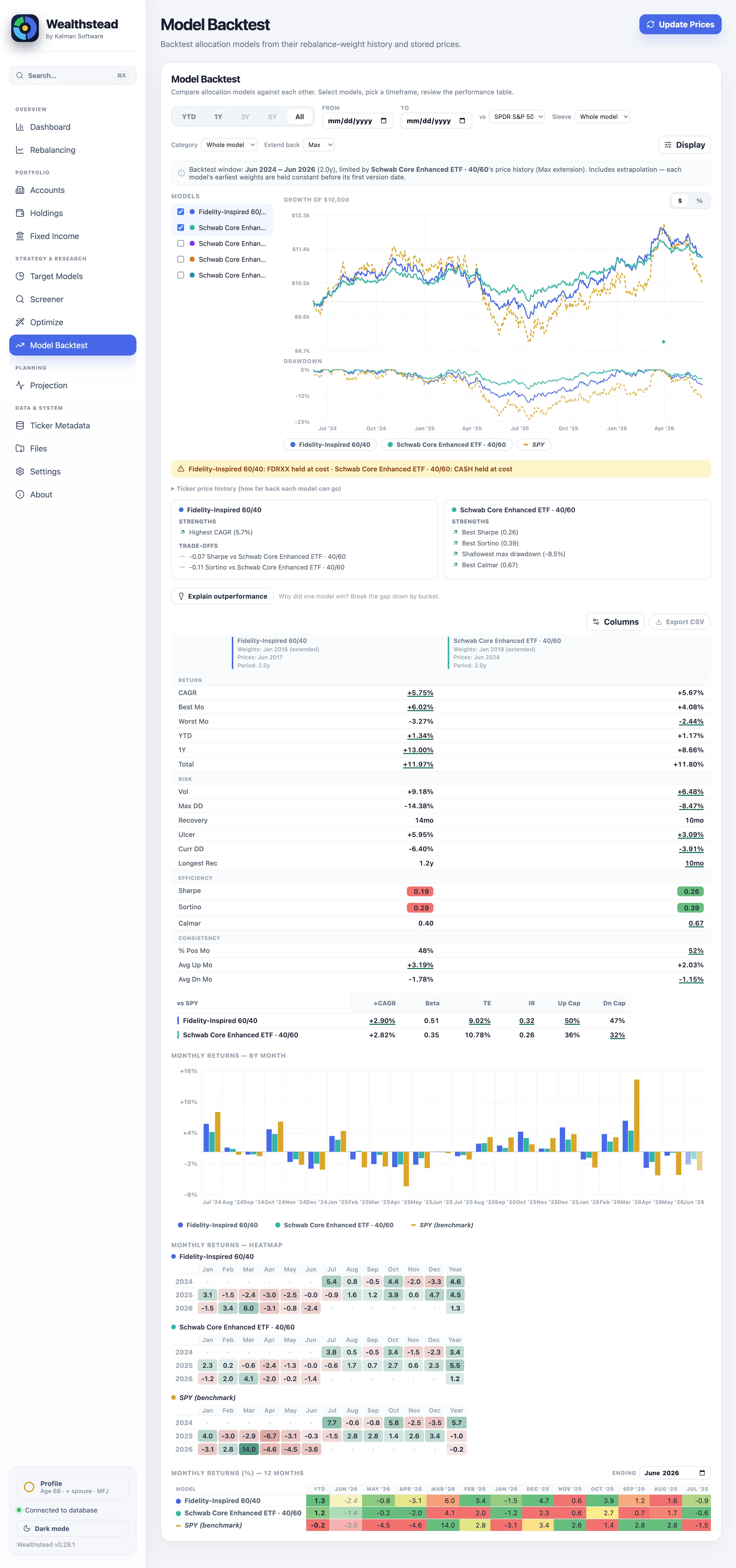

Before you commit money to a model — yours, or the one an advisor is charging you 1% for — replay it against history and read the result like a tearsheet. Compare several models at once over the honest common window:

| Model | CAGR | Volatility | Max DD | Total |

|---|---|---|---|---|

| Fidelity-Inspired 60/40 | 5.75% | 9.18% | −14.38% | +11.97% |

| Schwab Core Enhanced ETF · 40/60 | 5.67% | 6.48% | −8.47% | +11.80% |

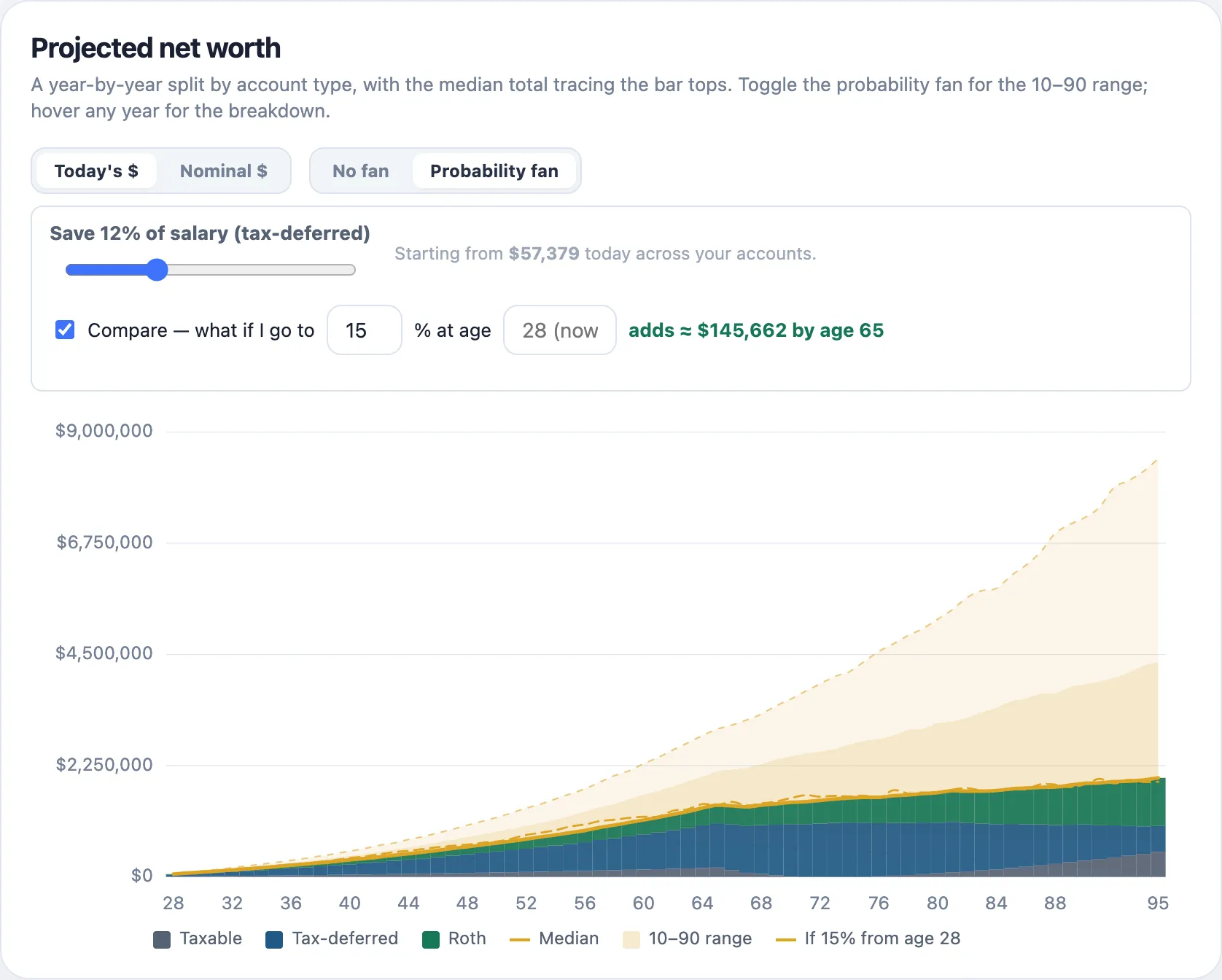

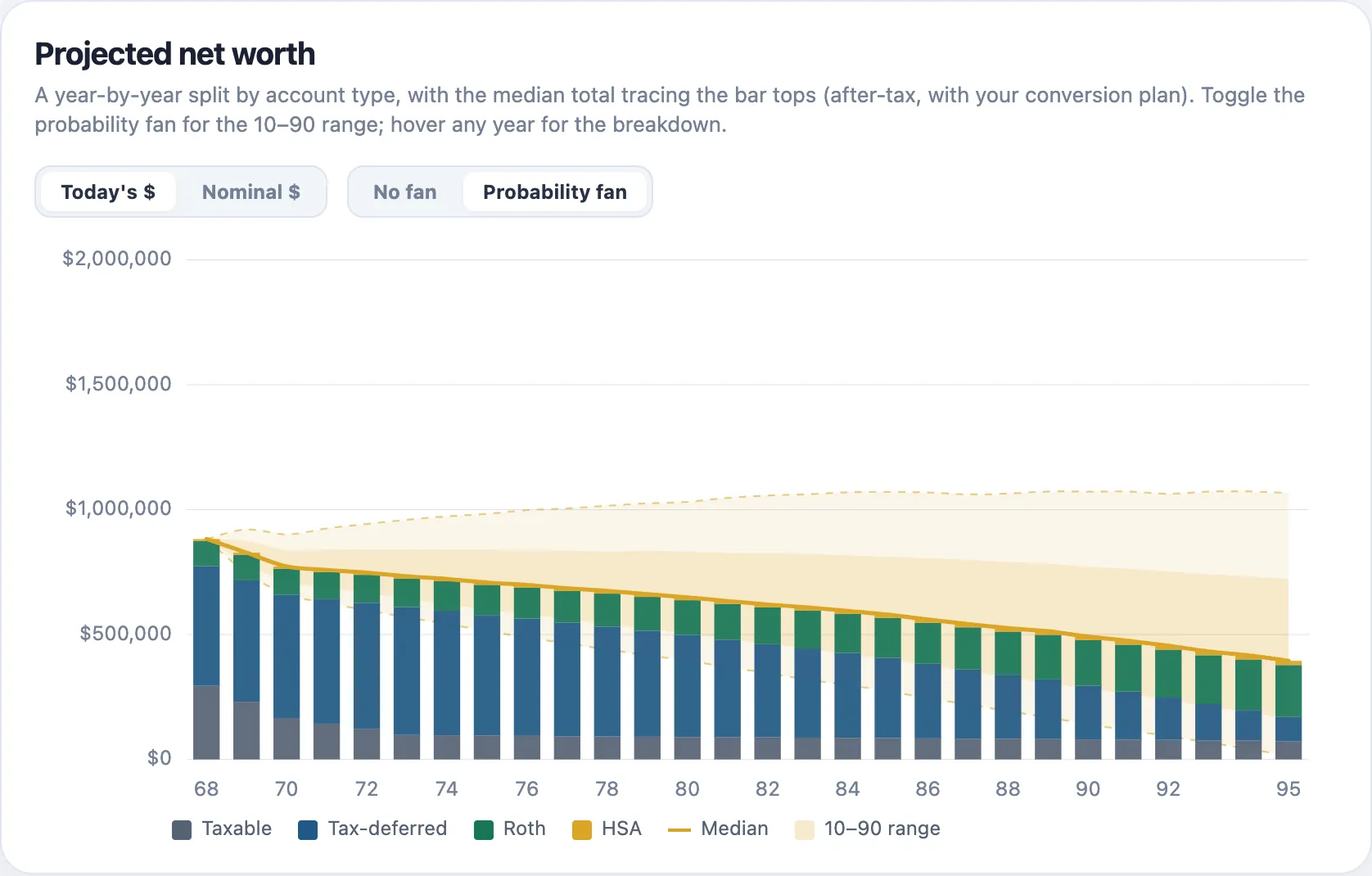

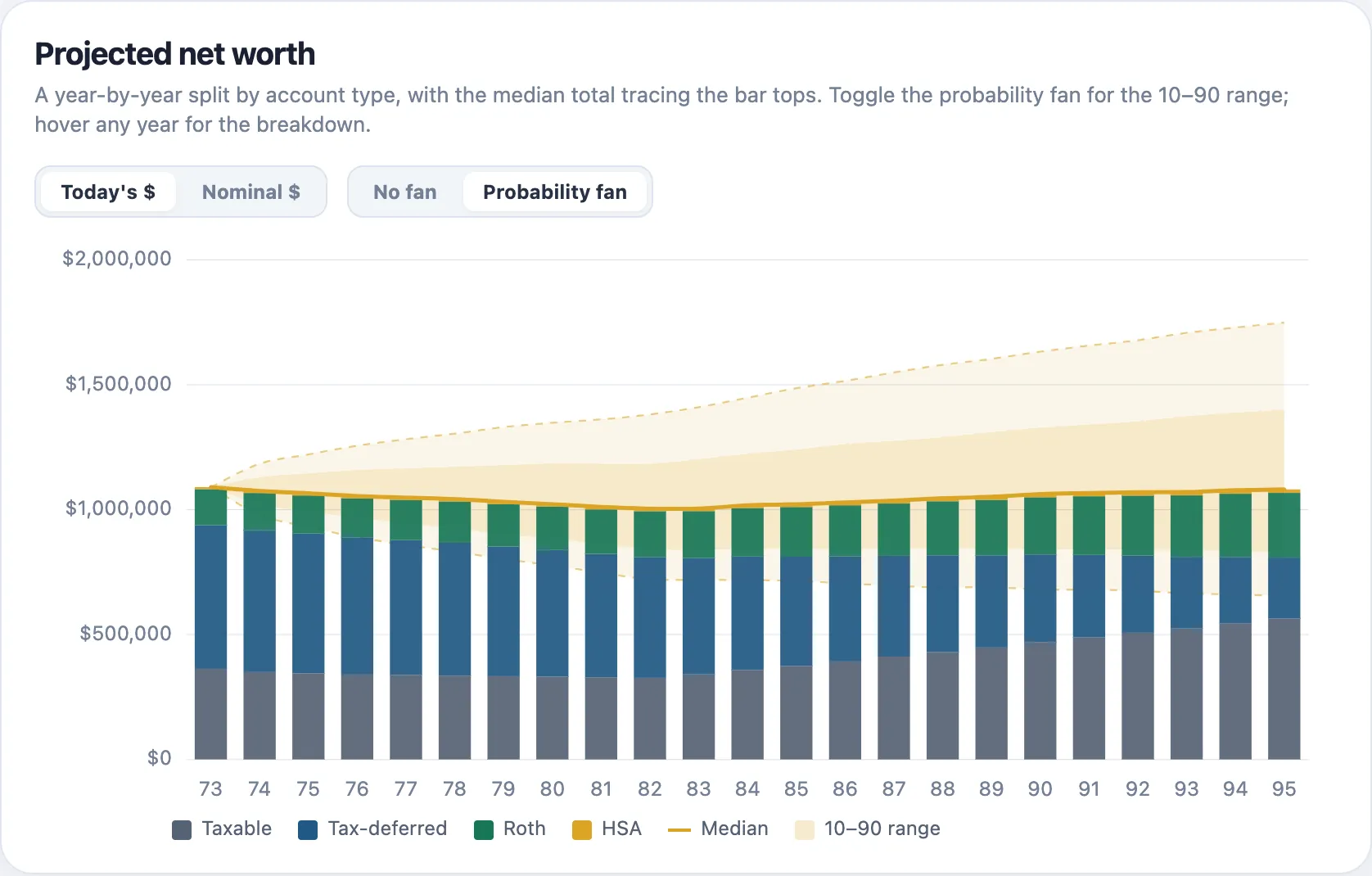

The question the whole loop exists for. Wealthstead runs a seeded Monte-Carlo projection of your entire household in today's dollars — starting from your real balances, split by tax treatment — and models the things that actually decide the answer: income and contributions while you work, spending in retirement, Social Security, per-owner RMDs, and real federal taxes, year by simulated year.

Four sample households ship with the app — one per life stage — so you can explore every scenario before touching your own data. Every figure below is real output from a deterministic run on these samples.

Fictional demo Four sample households (≈$57k / $352k / $882k / $1.09M) ship with the app. Every number here is read from a deterministic run on those samples, and every chart is a real capture. Reproduce any of it: Files → load a sample → open Projection.

Most planners quietly pick one return model and hand you a single confident number. Wealthstead scores the same plan three ways, side by side — because the spread between them tells you how much your plan leans on one reading of history.

Real output from a sample run: 86.6% under Forward · Normal, 85.9% under fat-tailed Student-t, 99.7% replaying 1928–2025. The 13-point spread is the finding — that plan was leaning on history's bond bull.

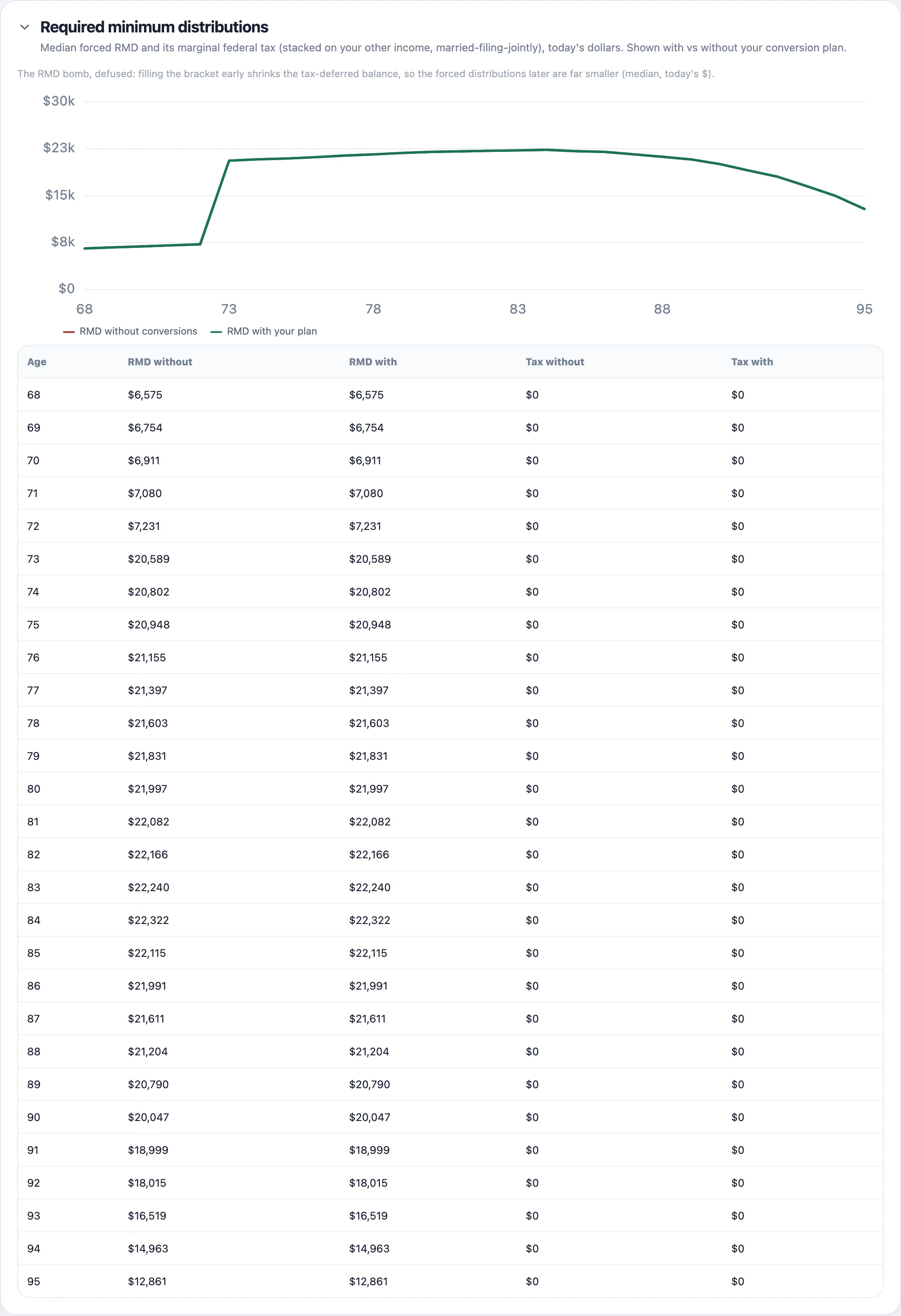

Every simulated year is taxed properly, in today's dollars — the projection knows a dollar in your IRA is not a dollar in your Roth. On top of that sits the optimizer retirees actually need: fill-to-bracket Roth conversions in the lean years between retiring and RMDs.

Retirement isn't one decision — it's a decade of them. The projection models the levers that decide whether the plan holds, including the one nobody likes to look at:

Every chart in this section is a real capture from a bundled sample — load it and you'll see the same thing.

A tool for your life savings should expect skepticism — and welcome it. Wealthstead earns trust by what it refuses to do, and by showing its work everywhere else.

Local-first by design: holdings, transactions, cost basis and plans are computed on your own machine and stored in a single file you can read, move and back up. There is no server to breach, subpoena, or shut down.

Every calculation runs locally. No server ever sees your accounts, balances or plans.

Open it and go. No sign-up, no cloud profile, no telemetry phoning home.

A single SQLite file — move it to a synced folder or a drive in your safe. Automatic timestamped backups. Zero lock-in.

One-time purchase, verified offline on your machine. No phone-home check, no server that can switch it off.

Whether you place every trade yourself or someone manages it for you, the promise is the same: a clear, private view of what you own, what it's doing, and where it's headed.

You run real multi-account portfolios at Fidelity, Schwab and beyond, and you want the full disciplined loop: a target, exact moves toward it, funds chosen on evidence, and a drawdown plan you've stress-tested.

Show me exactly what to place — and let me place it.

Enter the funds your advisor holds and see the allocation, performance and risk for yourself. Backtest their model against a three-fund alternative — and enter the fee to see exactly what it costs your outcome.

I want to understand — and question — what I'm paying for.

One click downloads the official daily share prices for all 16 TSP funds — G, F, C, S, I and every Lifecycle fund — so your Thrift Savings Plan sits as real holdings next to every brokerage account: tracked, compared, backtested, projected.

Put my whole plan — TSP included — on one screen.

Wealthstead began as a pile of spreadsheets — one engineer's, tuned and "improved" for years. The answers were all in there — are we balanced, what needs adjusting, will it last — just scattered across the sheets, and legible mostly to the person who built them. Retirement brought time to learn some new code, so the spreadsheets became an app: first just rebalancing, kept simple; then the whole collection in one interface easy enough that his wife could run the plan without him; then versions of it to help his adult kids get started.

It's still built that way: one person, running it on his own real portfolio, every week. No venture capital, no growth team, no data to harvest — just a tool its maker needs to be correct.

| Capability | Typical tracker or planner | Wealthstead |

|---|---|---|

| The output | "You're overweight equities" | "Add to the bond sleeve here, reduce the off-model AAPL there" — illustrative, to the dollar, per account |

| Your accounts | One account, or a linked login you have to trust | Every account — TSP, 401(k), IRAs, HSA, taxable — with no credentials, ever |

| Choosing funds | Star ratings and guesswork | A tunable, risk-adjusted Score across your NTF universe, plus a whole-model optimizer |

| Backtesting | One growth curve, if that | A full tearsheet with benchmark stats, drawdowns and honest data windows |

| Retirement math | One bell curve, one confident number | Three return models side by side — the spread is part of the answer |

| Planning depth | A 4%-rule slider | Real taxes, per-owner RMDs, Roth-conversion and affordability optimizers, a spending guardrail, a survivorship model |

| Bonds & CDs | Ignored, or marked to $0 | A real T-bill/CD ladder priced by accrual, counted in rebalancing |

| Your data | On someone else's server, feeding someone else's model | One local file on your machine, backed up on your terms |

| The business model | $8–$40 every month, forever | One-time license. The math doesn't expire, so the price shouldn't renew |

The big loop is backed by the small correctness that makes it trustworthy.

Performance that neutralizes your deposit timing — measuring the portfolio, not your cash-flow luck.

All 16 TSP funds with full official price history from tsp.gov — 56,566 rows back to 2003, added with one click.

Licensed Tiingo data as the shipping default, plus a free Yahoo Finance opt-in — pin a source per ticker, with a clean full-history rebuild on change.

Effective-dated model versions drive today's trades and yesterday's backtests — every change a marker on the chart.

Enter your broker's actual share count and Wealthstead writes the exact adjusting trade to make the ledger agree.

For accounts you don't track trade-by-trade, store periodic stated holdings — valued with Modified-Dietz returns.

Fix a split your data source missed with a date and ratio — corrected at read time, the download never mutated.

Multi-asset glide paths, Student-t fat tails, historical-sequence replay and AR(1) inflation — calibrated and tested.

Automatic timestamped backups on launch with a configurable keep-count, plus on-demand backup, restore, delete.

Wealthstead is in private build-out — here's what it will cost at launch, and how to lock the early-bird price today. Software that guards your money for decades shouldn't charge you rent for it.

Nothing to pay today — the app isn't downloadable yet. Join the early-access list and the $99 early-bird price is locked in for you before it rises to $149 at general release.

One email when it ships, with your download and the locked price. No list-building, no drip campaign — it goes straight to the person who built it.

Wealthstead runs on your machine and your portfolio lives in a file you control. Renting you access to your own plan would miss the whole point.

A one-time license — $99 early-bird at launch (regular $149), no subscription — with a 30-day free trial. The license is perpetual for the current major version. macOS and Linux ship at launch, with Windows to follow — join the Windows list and you'll be emailed as soon as it's ready. It's in private build-out now — join the early-access list and the download comes the moment it's ready.

No — and that's by design. You import a CSV transaction export from Fidelity or Schwab, or type in your monthly statement. Wealthstead never has your login, never moves money, and never places a trade. It shows illustrative Add / Reduce moves toward the target you set; you place every order yourself.

In a single SQLite file on your own machine. There's no cloud, no account, and no telemetry. You can see exactly where the file lives, move it to a synced folder or external drive, and keep automatic timestamped backups.

Yes — first-class. One click downloads the official daily share prices for all 16 TSP funds — G, F, C, S, I and every Lifecycle (L) fund — with full history from tsp.gov, back to 2003. Your TSP sits as real holdings next to your brokerage accounts: tracked, compared, backtested and included in the retirement projection.

No. Wealthstead is a calculator for a plan you design — it shows illustrative Add / Reduce moves toward the target allocation you set, and hypothetical projections from assumptions you enter. It is not financial, investment, or tax advice, and it doesn't recommend securities. Confirm prices, tax lots, wash-sale rules and suitability with your broker or advisor before acting; the app carries the same note at the point of each result.

The CSV importer auto-detects Fidelity and Schwab formats, and brokerage-aware ordering plus NTF (no-transaction-fee) filtering cover both. The model layer itself is brokerage-agnostic — implement the same target with whatever tickers you hold, wherever you hold them.

Yes — it's the whole second half of the app. The Projection runs a seeded Monte-Carlo simulation of your household in today's dollars, starting from your real balances by tax class. It models working-years contributions, spending phases, Social Security, one-time flows, taxes (federal brackets, a flat state rate, the Social-Security provisional worksheet, ACA/IRMAA ceilings) and per-owner RMDs. On top sit the optimizers: fill-to-bracket Roth conversions, a "when can I retire?" age sweep, a home-affordability frontier, a spending guardrail that flexes only the spending you've marked discretionary, and a survivorship model that shows the widow's penalty honestly.

Because one number would be pretending. The same plan is scored under a forward Normal model, a fat-tailed Student-t model, and a historical replay of 1928–2025 — and the historical replay itself offers four sampling methods, because how you reuse history quietly decides the answer. The spread between the lenses tells you how much your plan depends on one lucky reading of the past. Most planners pick one method and hide the choice; Wealthstead shows you the range.

Deliberately so. It runs in today's (real) dollars, so Social Security and tax brackets are treated as inflation-indexed rather than double-counted. It's seeded and deterministic, so optimizer comparisons are never sampling noise. The tax model is ordinary-income only — no LTCG/NIIT stack — a simplification documented right on the reference panel. Where a number can't be precise, the app says so instead of implying false confidence.

It's a risk-adjusted, Sharpe-like ranking: blended multi-period returns clear a risk-free hurdle, get divided by volatility, shrunk by how much history backs them, and penalized for expense ratio, max drawdown and year-to-year inconsistency. Every weight is tunable in Settings and the rankings update instantly. The Optimizer uses the same composite scoring to rank substitution candidates across every bucket at once.

They apply the model-weight version actually in force on each rebalance date, hold cash sleeves flat instead of redistributing them, and state the true common data window — presets the data can't cover are disabled, not silently truncated. Extending a backtest past a model's first version date discloses the extrapolation on the banner, and every statistic follows the window the chart shows. You can also overlay any ticker — a target-date fund, say — or another model as a benchmark, with excess CAGR, beta, tracking error, information ratio and up/down capture.

Held-to-maturity Treasuries, brokered CDs and bonds live in a Fixed Income view priced by accrual toward par — no fake $0 prices, no false dips on your value chart. You get the ladder by maturity date, FDIC issuer exposure, a forward income calendar, and a Builder that models a target ladder off the live Treasury par-yield curve. A model's ladder bucket counts every held rung in rebalancing automatically.

The shipping app uses Tiingo, a properly licensed market-data provider, plus official tsp.gov data for TSP funds. "Update prices" grabs only the missing recent days; "Rebuild" re-downloads from scratch. An optional Yahoo/yfinance source exists as an off-by-default, personal-use opt-in, and you can pin a source per ticker.

See what you own, get the exact moves toward what you want, and find out — honestly — whether it lasts. All on your own machine, all yours to keep.

In private build-out now — a one-time $99 early-bird license (regular $149) with a 30-day free trial. macOS & Linux at launch; Windows to follow. One email when it ships, straight from the builder.

Made by Kalman Software — indie, local-first, no VC, no data harvesting.